Irs Useful Life Of Solar Panels

Energy Efficiency Tax Rebates Energy Efficiency Solar Energy Solar Energy Companies

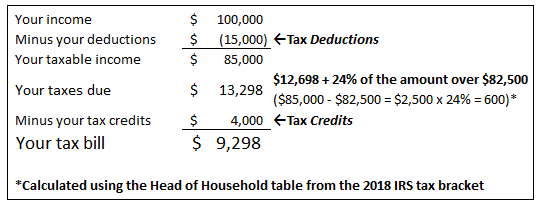

Pin On Do

Guide To Irs Form 5695 How To Claim The Federal Solar Tax Credit

5 Easy Ways To Prepare For Next Tax Season Money Talks News Tax Help Tax Write Offs Tax Return

Pin By Unique On Work From Home Uk Financial Coach Business Funding Business Finance

Commercial Depreciation On A Solar Energy System Yellowlite

That means at least 25 years of free electricity.

Irs useful life of solar panels.

An Introduction To Solar Depreciation Yellowlite

Mind Melting Facts About The Sun Nasa Jpl Infographics Energy Facts Educational Infographic Infographic

Governmentshutdown Zombies Apocalypse With Images Zombie Apocolypse Zombie Apocalypse Zombie Zone

Pin On Fare

The Tenants Of Semi Classical Gravity There Are A Number Of Hypotheses Running Around Trying To Reconcile General Relativity Quantum Physics Quantum Mechanics

2020 Guide To Solar Tax Credit Rebates And Other Incentives

Make Your Own Crude Shaking Torch Emergency Flashlight Emergency Flashlight Flashlight Electrical Projects

Youtube Roof Repair Panel Siding Repair

Yes You Re In The Right Place If You Need Any Fake Docs Passports Id Cards And Lots More To Get The Additional Information And P Utility Bill Gas Bill Bills

The Definitive Guide To Paying Taxes As A Real Estate Agent Aceableagent

Https Www Cmu Edu Ceic Assets Docs Publications Reports 2019 Ceic 19 04 The Value Of Solar For Peco And Its Ratepayers Pdf

Pin On Home Decoration Romantic Light

Tax Deductions For Rv Owners A Fulltime Rver S Personal Experience And Advice Tax Deductions Buying An Rv Deduction

Recycled Wastewater Infographic Reclaimed Water Water Pollution Water Facts

نصب بازار Qr Code Coding

Best Hris Software Human Resource Information System In 2016 Human Resources Human Resource Management System Workforce Management

How This New App Can Help You Track Miles With Images

Pin On Interests Fun Entertainment

The Superior Sports Network Play Of The Game Bamastate V S Alcorn Sta Networking Games Sports

Pin On Freedom S Guide Trading Company

Https Www Irs Gov Pub Irs Prior I1040 2010 Pdf

Pin On Make Money Online

10 Reason To Choose A Fifth Wheel For Full Time Rving Best Brake Pads Fifth Wheel Brake Pads

Art And Crafts Enjoy Coffee Arts And Crafts Coffee Sale

Source : pinterest.com